Use the latest browser recommended by Microsoft

Get speed, security and privacy with Microsoft Edge

Barbados’ payment habits continue to migrate from cash and cheques to faster electronic methods. The Central Bank’s Digital Payments Index signals broad adoption of digital options.

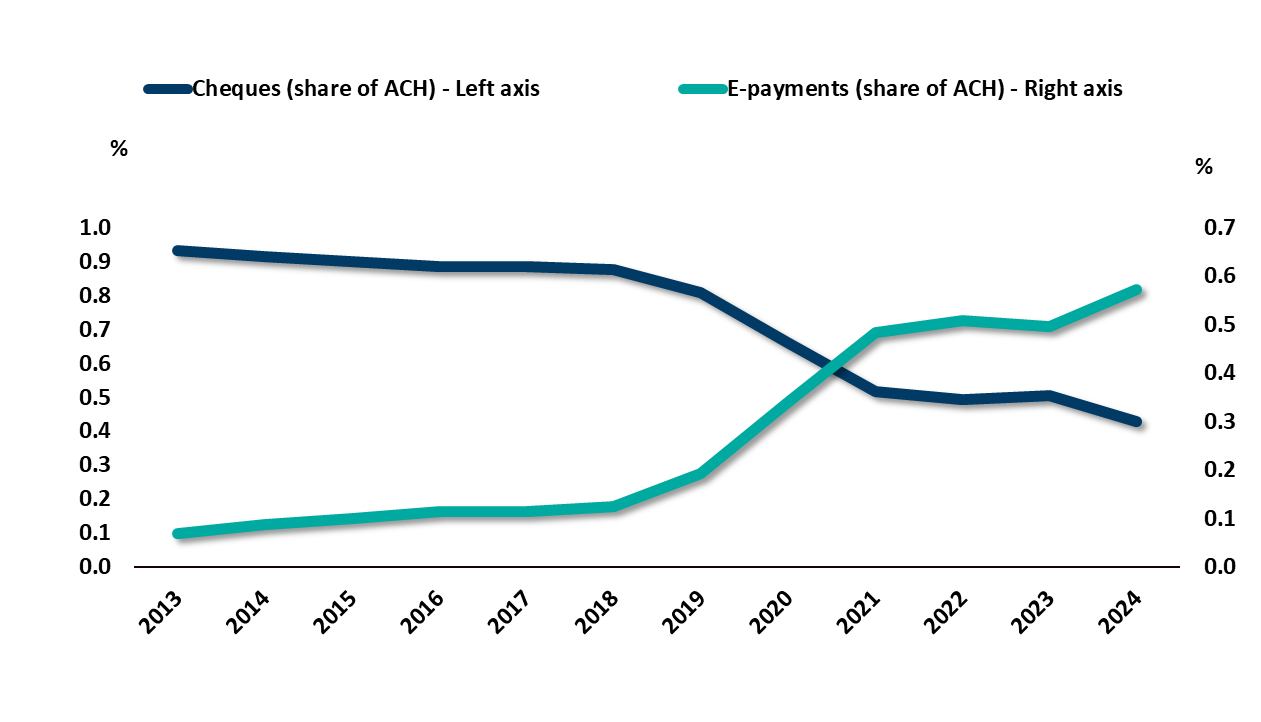

Cheque share in automated clearing house transactions fell by more than half over the last decade, while direct electronic transfers expanded by more than 700 percent. The point-of-sale share of debit transactions increased by 27 percent between 2013 and 2021, and the ATM share declined by 17 percent. Currency in circulation outside deposit-taking institutions fell in real terms by about 41 percent since 2013. Together these shifts confirm a structural move toward electronic payments.

The Digital Payments Index (DPI) provides a concise gauge of modernisation. The Bank combines six inflation-adjusted per-capita payment indicators as follows. Point-of-sale transactions, direct automated clearing house transfers[1], and credit card use signal greater digital uptake, while cheque volumes, ATM withdrawals, and currency in circulation serve as cash-based counter signals. The series are standardised[2] and averaged into a single summary indicator[3] that tracks the economy’s shift from cash reliance to digital adoption.

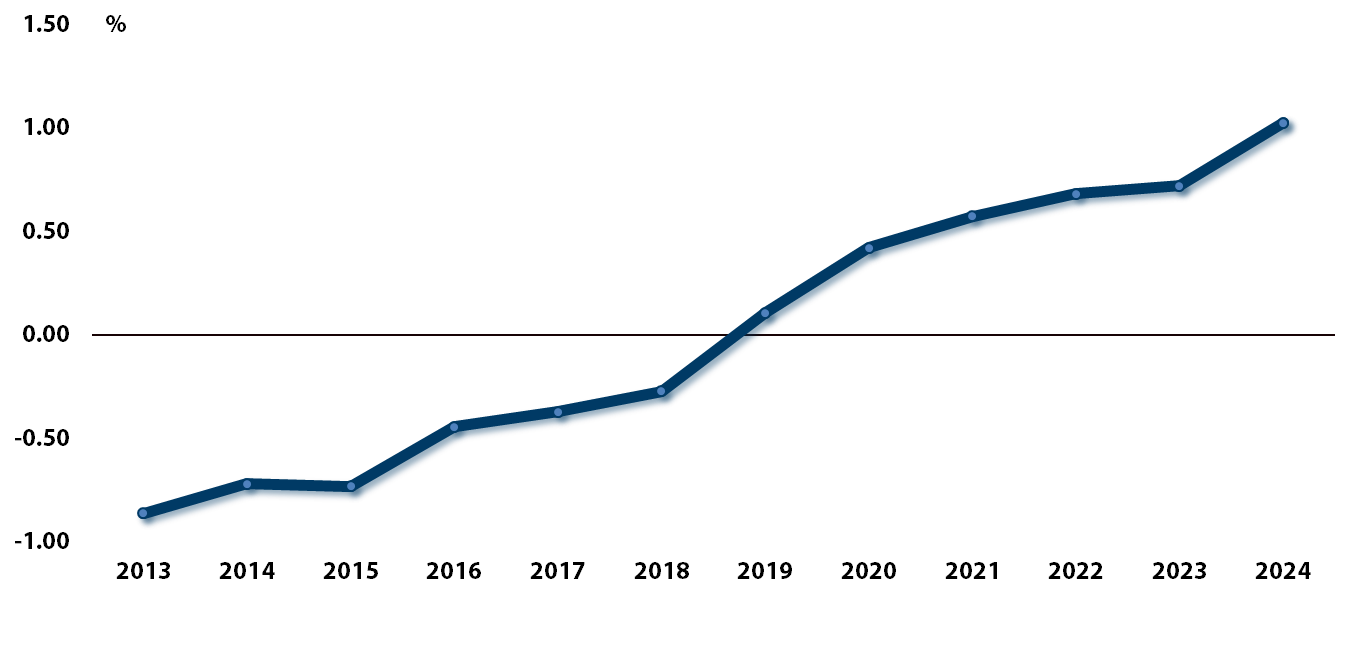

Electronic payments displaced cash and paper instruments from 2013 to 2024, lifting the DPI from -0.86 to +1.03, a gain of 1.89 standard deviations, as consumers and firms shifted to electronic channels. The index turned positive in 2019, the first-year electronic payments surpassed traditional methods. Pandemic restrictions accelerated adoption, and the pattern continued after restrictions ended, confirming a structural change in how Barbadians pay. Figure 1A traces this transition. An ongoing structural shift in payment behaviour shows up in three areas:

Together, these changes confirm a broad rebalancing of payment activity, from physical instruments toward electronic options, in line with trends across both advanced and emerging economies.

The Bank launched BiMPay in August 2025 with a go-live date of March 31, 2026. BiMPay delivers instant payments at any hour, moving funds within seconds between banks and licensed providers. The design promotes inclusion, since individuals, businesses, and government agencies can access the system, and persons without a traditional bank account can enter through participating institutions. Mandatory participation by core institutions secures coverage from launch, and the Central Bank of Barbados Act, the National Payment System Act 2021, and the new Regulatory Framework for Payment Service Providers[4] provide oversight that protects safety, efficiency, and resilience.

Even with rapid digital uptake, cash continues to play a trusted role in smaller transactions and for persons who prefer traditional methods. Policy therefore supports choice while encouraging safe and efficient digital options.

Sustained progress depends on strong public trust, robust cybersecurity, and wider merchant acceptance so that the benefits reach every user. With BiMPay scheduled to come on stream in 2026, Barbados joins peers that already offer real time instant payments, including Brazil, India, and the United Kingdom, advancing national goals of efficiency, inclusion, and financial stability.

[1] Automated clearing house (ACH) is an electronic funds transfer system used for batch processing of payments, typically taking one to three business days.

[2] A z-score (also called a standard score) shows how far and in what direction a single value is from its average, measured in standard deviations. A value of 0 means average; positive scores are above average, and negative scores are below average.

[3] OECD and European Commission, Joint Research Centre (JRC). Handbook on Constructing Composite Indicators: Methodology and User Guide. Paris: OECD Publishing, 2008. Handbook on Constructing Composite Indicators: Methodology and User Guide (EN)

[4] See here for details: Central Bank of Barbados Releases New Regulatory Framework for Payment Service Providers.

[5] Bank for International Settlements (2022). “Central banks, the monetary system and public payment infrastructures: lessons from Brazil’s Pix”. BIS Bulletin No. 52.

[6] Bank for International Settlements (2024). “The organisation of digital payments in India – lessons from the Unified Payments Interface (UPI)”. BIS Papers No. 152.

Source: Central Bank of Barbados

Source: Central Bank of Barbados